The custom install channel is right in the middle of buying group season. ProSource took place at the beginning of March, HTSA will be held in Nashville in mid April, and I just returned from the well-attended Spring Soiree in Nashville, hosted by Azione Unlimited, a buying group that seems to be hitting its stride.

The youngest of the three groups (not including ProSource which was reformed and renamed after a merger), Azione began modestly in 2011 by former HTSA director Richard Glikes after he parted ways with HTSA. That forgettable upstart is now a viable player in the market, having grown its membership to 111 members, while adding new vendor partners seemingly every month (that total is up to about 50, with Sony and Screen Innovations as the two newest members).

Richard Glikes, Azione Unlimited founder

Perhaps the most “custom-centric” of the major buying groups, Azione features a blend of well-known CIs and many fresh faces from the industry that, while maybe not new to the industry, are less known players from smaller markets in the country. It makes for a good blend of personalities, with the veterans willing to share insight with the newbies and vice versa. All Azione dealers pay $3,000 annual dues to members of the group. The manufacturers have a voice in the group’s board, which is unique for the channel. Although it feels to me that Azione has truly “arrived” as a legitimate player in the market, Glikes says that he’s nowhere near his goal in developing the group membership, stating his goal of having 250 members and his hopes for rounding out some of its product offerings.

Glikes runs a tight meeting, with his legendary refrain, “The time is the time” guiding the pace of sessions. Presentations are kept short, and interaction between members that don’t already know each other is greatly encouraged.

On Tuesday, the dealer-only portion of the event commenced with a general state of the industry report, in which Glikes confirmed with those in the room that “business is good” and that the era of “building the big house” is back. He noted, however, that technology “change is coming faster than ever” with margins dropping in many categories. That, he said, should encourage integrators to charge higher labor rates (between 35-40 percent of the total ticket price) because “service is the key” and “it’s the one thing that is always scarce.” After staffing cutbacks from 2007-2009, almost every integrator has fewer and sometimes less-qualified installers on their team, and those staff members will be even harder to find as the employment rate continues to drop in the U.S.

“You’re going to have to pay your people more when our employment rate (which is now 5.5 percent) drops to five percent,” Glikes said.

Glikes also noted that every vendor in the control category wants to diversify, noting that even Staples (“a paper company”) is selling home automation and that Samsung is working on a project that embeds a tiny chip in all of its TVs to add more intuitive control.

Dave Pedigo, CEDIA

Other sessions were led by last year’s CEDIA Lifetime Achievement Award winner Frank White, an industry consultant that shared his perspective on building a proper “org chart” for an integration company, as well as business coach Peter Sieffert from San Diego’s Swiss Ave Partners, and a panel on “effectively working with builders,” featuring dealers Scott Bekendorfer, Rocky McCarthy, Mark Ontiveros, Bill Charney, and Don Dixon.

CEDIA’s senior director of learning and emerging technologies, Dave Pedigo, also presented sessions on CEDIA’s market survey results as well as his opinions on the top five technology trends. He focused on the evolving video display types or capabilities (high dynamic range, wider color space, OLED and Quantum Dots, 8K, curved TVs, and ultra short throw projection.) He also discussed streaming trends and the potential for new connector types (super MHL) and a new version of HDMI for 4K and 8K resolutions. He offered some insight into the connected “luminares” space (essentially controllable light bulbs) and how this is an opportunity for integrators. He also highlighted the 3D audio trend, which includes Dolby Atmos, Auro3D, and DTS:X, IP-based home automation, and the Internet of Things trend.

Pedigo’s strongest words of advice for integrators had to do with the growing number of IoT and mass-market home automation threats. “Sell yourself as the expert on these topics because there is so much confusion and the user experience is not that great,” he stated. “These products work okay 85 percent of the time, but is that acceptable to your clients? It’s not. All of the marketing is being done for you. Consumers want it, but it’s your job to explain why DIY is not all that it’s cracked up to be.

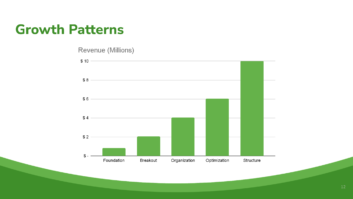

In his review of market data from CEDIA’s State of the Industry survey, Pedigo said that “the industry is really really strong,” up 37.8 percent in annual gross revenue from two years ago. The industry, he said, is up in almost every category. The average number of projects is going up, and the dollar amount is going up disproportionately more, meaning that each project has a bigger budget than before. Home theater, he said, is back to 22 percent of total gross revenue (it had dropped to 17 percent, having reached its peak at 23 percent in 2007. Distributed AV has remains steady (17 percent) as the second largest category, even facing “commoditized disruption.” Control systems are at 12-15 percent, which has been stable for years, distributed video nine percent, and lighting control six percent. IT/Networking is an area of growth, having moved to six percent from only one percent. Outdoor categories increased as well, while structured wiring declined, and not much changed for the smaller motorized shades category (which surprised Pedigo the most.)

In one of Sieffert’s two sessions, he showed how to use an interesting management tools that his company offers to business owners. I’ll explain it in more detail in my next editor’s letter, but it’s called “RGBY” for “red, green, blue, yellow,” and it helps an owner or top-level manager better divide up the many roles and responsibilities in his company to clear his brain space and cluttered desk of task that prevent him or her from blue sky thinking and increasing the value of the business for resale.

Most owners, he said, tend to spend time on the wrong areas of their company, constantly putting out fires instead. RGBY helps an owner create the structure to necessary to hand off activities and tasks to his or her staff.

Azione’s 2014 Dealer Business Doublers

During its awards presentation, Azione Unlimited provided the following members with honors:

2014 Champion Member: Mark Ontiveros

Bulldog Award: Dennis Jaques

2014 S.P.I.K.E. Award (supportive, profitable, invested, killing it, engaged): Starr Systems Design and Middle Atlantic

2014 Most Growth: Cantara

Golden Goose Q4-2014: Samsung

2014 Outstanding Support: Integra and Triad Speakers

2014 Vendor of the Year: Savant

Product of the Year: Sonance Digital Amps

Dealer Business Doublers 2014: Advanced Integrated Systems, Advanced Home Theater, Audio High, Cantara, Easy Living with Technology, Experience Technology, Hermary’s, Lava, Media Design Associates, Opus AVC, Residential Systems, Sound Ideas, Starr Systems, Audio Warehouse, Tunnel Vision, Xssentials

Vendor Business Doublers 2014: IC Realtime and Netsertive

Vendor Business Tripler 2014: Meridian