We’re busy. And if we were forced to reduce the state of the industry to two words, those would be it. However, we’ve got many more words than that, and while busy is great and you are no doubt aware of how your business has fared this year, it is interesting to look at the industry as a whole — not just to see if your business is tracking with others — but also to take a snapshot of where we are and what we’ve recently experienced.

This is our third year of working with Portal to look at what dealers are specifying in aggregate to get an overview of what’s happening in the industry. We started in 2020, noting the brief April slowdown and the following rapid rise of business as the pandemic took hold. In last year’s story, we could see the industry continued to grow, although not as steeply as it had in 2020. Can that trend continue?

Once again, Portal founder and CEO Kirk Chisholm and COO Josh Willits have provided some insights from the aggregate sales data in Portal. (Willits has also once again accounted for Portal’s growth over the past year and removed that data for the comparisons to the previous year.)

In terms of the number of jobs being specified, Chisholm notices a slight uptick. “This year the number of jobs each month averages out to about six, whereas before it was five and a half,” he says. “It’s only half a proposal a month, but it’s one new proposal they’re adding every two months. It all adds up.”

Beware the Bear

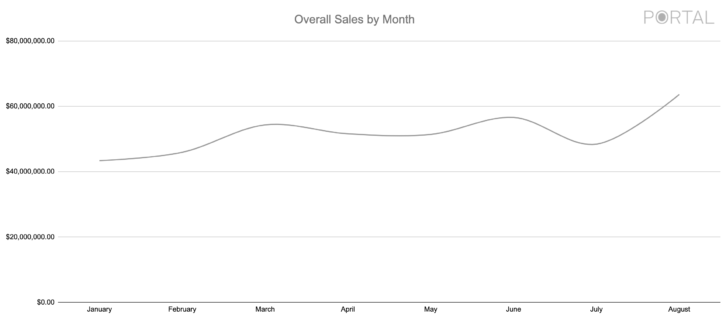

Figure 1 represents overall 2022 sales displayed month-over-month. Growth has slowed, but it is still there, with a nice jump from January to March, holding mostly steady through June, followed by a sharp drop in July with a quick rebound through August.

That drop in July can be seen throughout the charts this year in nearly every product category. In speaking anecdotally with manufacturers and dealers about their businesses, several saw the same midsummer drop. Although no one we spoke with could pinpoint a definitive reason for the loss, common suspects were the return of families going away for summer vacation, keeping us out of their homes, and trouble in the stock market.

In June 2022, the U.S. stock market entered a bear market for the first time since March 2020, which happens when the stocks fall at least 20 percent from their peak. The drop in July could be explained by clients becoming more cautious to see how things played out. The rise in August shows optimism even in the face of a continuing volatile market.

The Year in Gear

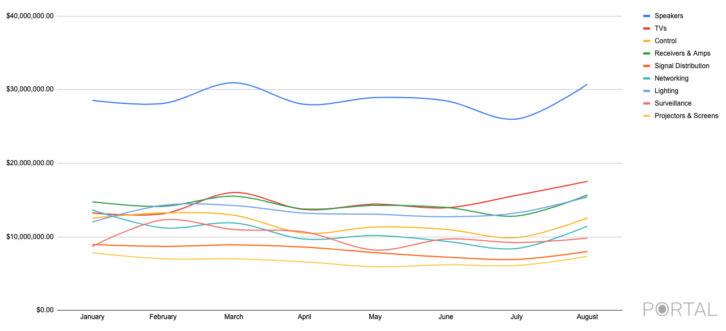

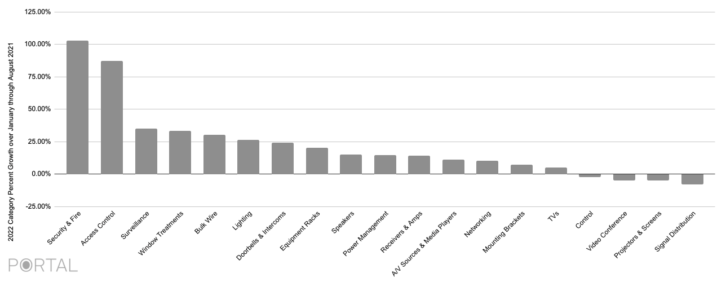

Figure 2 shows the top categories being specified. Like last year, the Speakers category is still on top by itself and reflects the July dip. “Receivers & Amplifiers and Lighting categories had strong 2022 growth compared to 2021 over the same months,” says Willits. “Signal Distribution took a hit in 2022 compared to 2021, and we saw a lot of growth in Security & Fire.”

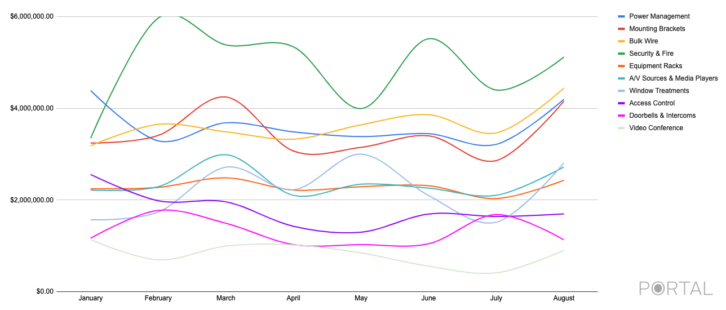

That growth in Security & Fire can be seen in Figure 3, which shows additional categories. Nearly all categories — except Access Control and Doorbells & Intercom — show the July dip.

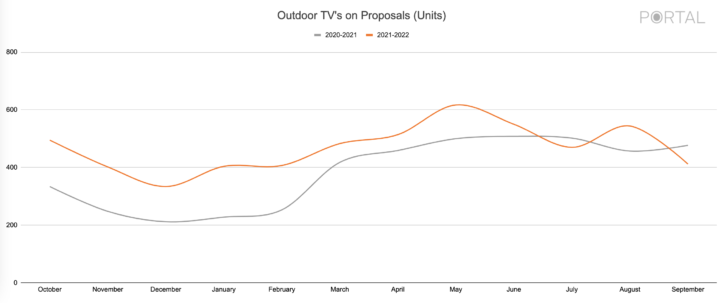

When we focus on outdoor televisions — a hot category for many integrators and shown in Figure 4 — we see this year outperformed last year until July, then recovered nicely only to have a seasonal decline that we didn’t see the past couple of years.

“This graph is interesting, as we can see the dip in July, which was category-wide on Portal, but, more importantly, September 2022 was below September 2021 despite 6 percent more dealers quoting TVs,” says Willits. “The growth of this category is stagnating going into Q4 2022.”

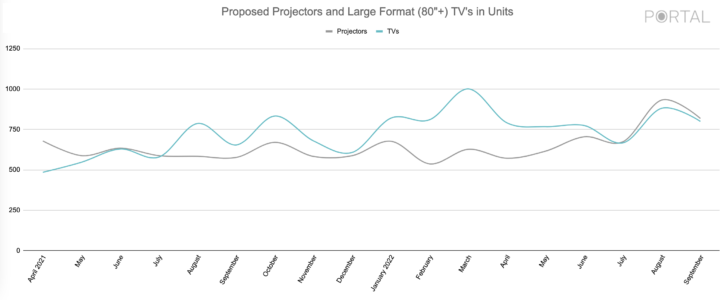

Figure 5 compares projectors to large-format televisions (80-plus inches) starting in April 2021. For the most part, TVs have dominated, although projectors came on strong from the July dip through September. There are a few reasons for this, Willits explains.

“This graph begins in April 2021, because there were some supply chain issues with projector screens that were pronounced in midsummer 2021,” he says. “We can see a trend line of fairly stagnant projectors through the entire period as the large-format TVs being specified are increasing over time. They did come back together almost unit-for-unit in July 2022 and have been very close for the last three months. As prices decrease for large-panel TVs, we do anticipate the separation will continue; however, projector manufacturers have created more competitive products with short-throw systems that perform well in higher ambient light rooms.”

Figure 6 shows growth per category, with the top spot going to Security & Fire, which points to expanded — or starting — security offerings for dealers.

A Second Perspective

Like last year, we also checked in with Jetbuilt founder and CEO Paul Dexter to see what its users were spec’ing and if it can corroborate Portal’s findings.

“I could start by stating the obvious: that integrators were busier this year as people were anxious to brush off the Covid cobwebs,” says Dexter. “Overall, our set quoted 9.4 percent more projects this year than last by quantity, meaning they are getting nearly 10 percent more calls for projects this year. While that is a somewhat traditional growth figure, we feel it is a strong number considering the fragility of the economy and inflation overall. This is the most unique recession we’ve ever seen, with both sales and staff increasing as we head into uncertainty. It will be very interesting to see how our set plays out this time next year.

“The average price of all projects quoted went up by 20 percent,” he continues. “This shows more spending per project, but with inflation, as it is, this figure reflects a bit of two causes.”

In terms of the product categories, the results are fairly similar to Portal’s findings: “Where TV sales grew sharply the previous two years, they fell flat this year,” says Dexter. “Literally down 11 percent among our set. This was not true for projectors, which continued to rise moderately for home theater use.

“Advanced control systems continue to make their way to the mainstream,” he adds. “While they saw a nice increase last year, they more than doubled in 2022. This follows the commercial trend from the last 10 years, where control systems became ubiquitous in that span. But in residential it took some time for the technology to reach the mainstream in terms of whole-home automation.

“The strongest outlier was Automated Shades. Where we reported nice gains last year, their sales tripled for our set of integrators in 2022. The cause could be coupled with the mentioned adoption of advanced control systems. Once you have central control of your audio and lighting, it is easy for an integrator to present the power and convenience of automated shades. Like we always see with consumer electronics — once the price comes out of the clouds, the more of your neighbors have them, and the more vendors jump into the market, they become the next go-to item for your home.

“Security and Surveillance spending doubled over the last year among this set of integrators. This points to more AV integrators crossing into that converging market. Over the last several years we saw them do that with networking, which only held its position over the last year. We saw several of our security-only installers make moves into AV, so clearly the AV teams are returning that idea.”

The Distributor View

From the distributor perspective, Cynthia Menna, vice president and general manager for AV at ADI Global Distribution, sees a growing trend in resimercial jobs. “We see more and more integrators cross between residential and commercial installations — and we’re helping them do just that,” she says. “Customers depend on our Systems Design Support, and our Herman Integration Services helps them take on more commercial jobs.”

In terms of the products ADI is providing, Menna says, “The trend of people investing more in their homes continues to carry on. The intrusion, smart home, and AV categories are growing as homeowners see the value in home entertainment and a connected home. Video doorbells, smart thermostats, speakers, lighting controls, and the systems and apps that drive them have become increasingly important to end customers. Additionally, we’re seeing more homeowners investing in networking, Wi-Fi, video bars, conferencing cameras, and technologies for home offices and hybrid working models.

“Outdoor entertainment categories have continued to gain popularity during the summer months and in warmer geographies. We’re seeing more outdoor TVs and audio installed around the pool, lounging areas, and firepits to provide a better and more leisurely entertainment area.

“As we expect the supply chain disruptions and uncertainties we’re seeing across the industry to continue into 2023, we’ll continue to take every step possible to try and lessen the impact for our customers.

“ADI has a strong supply chain and logistics operation, and we’re focused on providing our customers with immediate access to the products they need when they need them. Many of our customers do not maintain a warehouse and prefer to buy per job to help improve their cash flow. ADI operates 115-plus branches and 10 strategically located distribution centers across North America, and our in-stock inventory levels allow dealers to carry little or no local inventory. Additionally, we have a dedicated demand planning team that regularly collaborates with our supplier partners and integrators to ensure that we have appropriate inventory levels.”

Requiem for the Middle Market?

While this all points toward growth for the industry, some warning signs are important to recognize. The stock market has not yet fully recovered and the housing market is in a strange state with high interest rates combined with inflation, which is making things difficult for buyers, sellers, and builders. And then there is the disappearing middle market.

Todd Anthony Puma and Mark Feinberg first called attention to the middle market’s woes in a March 2022 Residential Systems blog titled, “Is the Middle Market Doomed?” In that piece, they explain: “Clients are starting to balk at the pricing as items have increased up to double in price in the past five years. We are seeing an erosion of the middle market — these clients just cannot afford the product we sell and are more likely to turn to DIY solutions such as Lutron Caseta lighting, Lutron Serena shades, Nest thermostats, August door locks, Arlo and Nest cameras, and so on. They are more willing to have multiple apps on their phones and less integration between subsystems because the price-value ratio just isn’t there for them. I understand, and if I were a consumer in this market, I’d probably feel the same way.”

They followed up those thoughts in an October 2022 blog, “The Shifting Market.” There, they state: “More and more we are noticing that our jobs are bifurcating. Our smaller jobs are getting a little bit smaller — they are on average about half the size of what they used to be, and our larger jobs are getting larger and have gone up in size by 25 to 50 percent. The middle seems to be disappearing.”

They continue: “Projects that typically would have been $40,000 to $50,000 are now $25,000 to $40,000. For Todd, that has come at the expense of some subsystems such as lighting and shading being pared back or de-scoping rooms. For Mark, it is often using a simpler and more consumer-oriented approach, like a smart TV and Sonos soundbar and subwoofer, obviating the need for a universal remote, eliminating the control system altogether (unless other smart home features are in play), and removing the costs of video distribution.” (This could partially explain the dip in signal distribution we noted earlier.)

Todd and Mark cover the N.Y.-N.J. area, so results may vary depending on where you live. Still, if a big portion of your business is in the middle market, you may look to diversify your jobs or better communicate the benefits of your services to your clientele versus DIY.

So, the last word on the state of the industry is the same as the first one…well, the first two…we’re busy — and it looks like that is a trend that will continue at least in the near future.

For more detailed, brand-specific sales data, manufacturers and distributors can contact [email protected].